LIC New Endowment Plan

Table of Contents

LIC New Endowment Plan is a non-linked, participating plan that offers an attractive combination of security and savings features. Offers guaranteed returns and bonuses. This is a traditional life insurance plan. You can take this endowment plan with the many benefits in mind. With its expert customer service, the LIC of India helps you get the best insurance policy according to your needs and suitability. You can choose the policy term from 12 to 35 years. Anyone between the ages of 8 and 55 can take this policy and it can continue for up to 75 years. You pay a premium for the entire term of the policy. This plan is included in the basic LIC plans that provide death and maturity benefits. The maturity benefit is equal to the Sum Assured plus the Simple Reversionary Bonus acquired + the Final Addition Bonus. Here you have everything you want to know.

| Plan No. | 932 |

| Launch Dated | 1 Feb 2020 |

Why we should buy this New Endowment Plan?

The New Endowment Plan is one of the best plans of LIC that offers both protection and saving features. The following are the key features that make it a perfect plan for young people.

- It assures you good returns and bonuses.

- It is one of the traditional plans of LIC.

- If the insured person dies before the maturity period, the nominee will get the death benefit and the policy will be terminated.

- It pays a good lump sum amount to the surviving policyholder at the end of the maturity period and then the policy terminates.

- It allows a flexible entry age from a minimum of 8 years to a maximum of 55 years.

- The policy premium can be paid through annually, half-yearly, quarterly or monthly installments.

- It provides to the policyholder through its loan facility in case of liquidity needs.

What are the benefits available for this New Endowment Plan?

-

Death Benefit

This plan offers the death benefit (sum assured) too, in terms of Simple Reversionary Bonus acquired and the Final Additional Bonus to the family of the insured in the event of the death of the insured during the term of the policy. Thereafter, the policy ends.

Provided that the policy includes “Sum insured in case of death”, where the given term is defined as greater than the basic sum insured or 10 times the annual premium with a minimum of 105% of the total premium paid.

-

Maturity Benefit

On survival of insured person till the maturity date, he/she will get the Basic Sum Assured with vested Simple Reversionary Bonus and Final Additional Bonus( if any) and the policy will then terminate.

-

Income Tax Benefit

The policyholder of this plan entertains a tax exemption up to Rs 1,50,000 under Section 80(C) of Income Tax act on the annual insurance premium to be paid and also the maturity amount is exempted from tax, terms, and conditions are there.

-

Participation in Profit

This New Endowment Plan of LIC also includes a share of the profit of the company. It gives Simple Reversionary Bonuses with Final Additional bonus, calculated on the basis of experience of the company, terms and conditions are there.

What are the Provisions and restrictions of this New Endowment Plan?

-

Entry Age

| Minimum | 8 years |

| Maximum | 55 years |

-

Basic Sum Assured (in Rs.)

| Minimum | 1,00,000 |

| Maximum | No Limit (multiple of 5000) |

-

Policy Term

| Minimum | 12 years |

| Maximum | 35 years |

-

Maturity Age

| Maximum | 75 years |

-

Monthly Premium (in Rs.)

| Minimum | 250 |

| Maximum | 10000 |

What will be the date of commencement of risk under the New Endowment Plan?

The risk will commence immediately on acceptance of the risk

What are the options available for this New Endowment Plan?

This plan has five optional riders when you pay an additional premium. A maximum of four riders one can avail of whereas the policyholder has to choose either LIC’s Accidental Death and Disability Benefit Rider or LIC’s accidental benefit rider.

The five riders are:

- Accidental Death and Disability Rider

- Accidental Benefit Rider

- New Critical Illness Benefit Rider

- New Term Assurance Rider

- Premium Waiver Benefit Rider

Sum assured under each rider cannot exceed the Basic Sum Assured under the policy.

For more details, please refer to the Rider Brochure on the LIC’s official website or contact the nearest branch of LIC.

What is the option to take Death Benefit in installments?

Yes, instead of taking the lump sum amount you can split it into a number of installments over a period of 5 or 10 or 15 years. The insured person will be paid the installments in advance at monthly or quarterly or half-yearly or yearly intervals.

The minimum installment amount for different intervals are:

| Mode of installment payment | Minimum Instalment Amount (in Rs.) |

| Yearly | 50000 |

| Half-yearly | 25000 |

| Quarterly | 15000 |

| Monthly | 5000 |

What is the Payment of Premiums mode available for this New Endowment Plan?

Premiums are to be paid at regular intervals such as monthly, quarterly, half-yearly, or yearly (through NACH only) or through salary deductions.

What is Grace Period for this New Endowment Plan?

In case the policyholder cannot pay the premium on time, a grace period of 30 days is available for yearly, half-yearly and quarterly payments whereas a 15 days grace period for monthly payments is available. If the premium is not paid before the expiry date of the grace period, the policy lapses.

Such grace period also covers the rider’s premiums along with the base policy premium.

What are the Rebates available for this plan?

-

Mode Rebate

| Yearly mode | 2% of Tabular Premium |

| Half-yearly mode | 1% of Tabular Premium |

| Quarterly, monthly and Salary Deduction | NIL |

-

Basic Sum Assured (B.S.A.) Rebate (in Rs.)

| 100000-195000 | NIL |

| 200000-495000 | 2% of B.S.A. |

| 500000 and above | 3% of B.S.A. |

What is Revival?

If the policyholder fails to pay the premium within the grace period and the policy lapses, then a revival period is also there. The revival period is of 5 consecutive years from the due date of first unpaid premium but before the date of maturity, as the case may be.

The revival of policy will come into effect only after the submission of all the due premiums with its interests compounding half-yearly at the rate fixed by the corporation from time to time and on the satisfaction of Continued Insurability of the life assured and/or proposer (if Premium Waiver Benefit Rider is opted for).

What is Paid-up Value?

If the premiums are paid regularly on time for at least two full policy years, and after that, any subsequent premium is not paid within the grace period, then the policy will not become wholly void but will subsist as a paid-up policy till the end of the policy term.

Such paid-up policy cannot participate in future profits but bonus remains attached to the reduced paid-up policy.

What is the Surrender Value?

After the payment of premiums without any lapse for at least two years, the policy can be surrendered with the interest of the policyholder and the corporation will pay the surrender value equal to higher of Guaranteed Surrender Value or Special Surrender Value.

If there is any bonus or rider opted for, it will be calculated on the basis of the ratio of Surrender Value.

What is Policy Loan?

After at least two full years premium have been paid, the loan can be granted under the policy subject to the terms and conditions of the corporation.

What is the Free Look Period?

In case the Policyholder has some personal problems or he is not satisfied with the terms and conditions of the policy, there is a Free Look Period of 15 days from the date of accepting the bond within which he/she has to return the policy to the corporation by citing the reason. Then the policy will be canceled and after deducting the processing charges, the premium will be returned.

What are the Exclusions?

- By the way, if the insured (whether sane or insane) commits suicide within 12 months from the date of commencement of risk. As a result, the corporation will not accept any claim on the policy. Only 80% of the total premium paid would be returned provided the policy is in force.

- Similarly, if the insured (whether sane or insane) commits suicide within 12 months from the date of revival then an amount that is higher of 80% of the total premiums paid till the date of death or the surrender value available as on the date of death shall be payable. The corporation will not entertain any other claim on this.

This clause will not be applicable for a lapsed policy without acquiring paid-up value and nothing will be paid under said policy.

Read to know more about this:

LIC की बहुत ही जबरदस्त स्कीम, 27 रुपये रोजाना करें निवेश, मिलेगा एकमुश्त 10.62 लाख।

Also, read this – Why is LIC’s New Jeevan Anand Plan the Best Choice for Young Couple?

")

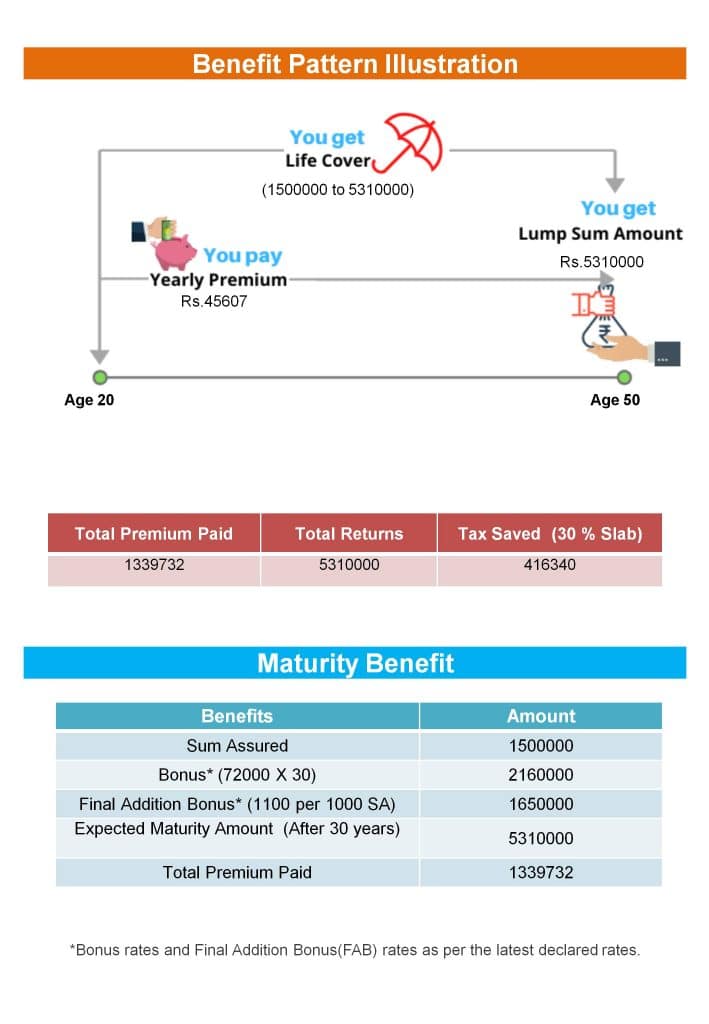

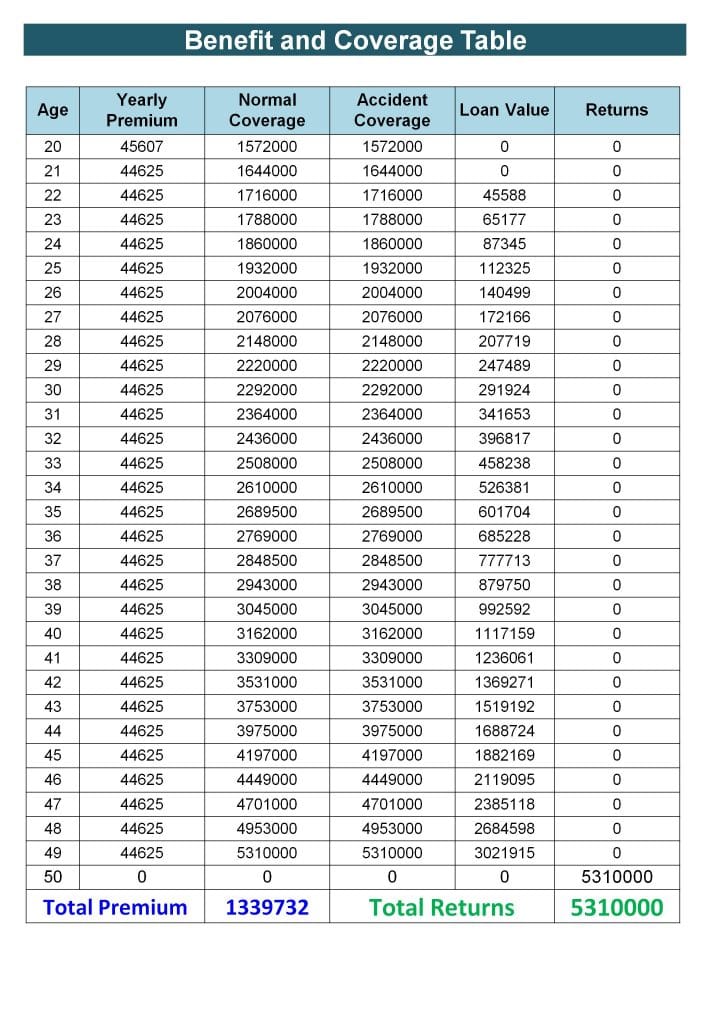

Plan Illustration

Disclaimer:

The Premium amount shown here is indicative and informational. The actual premium amount can vary according to underwriting rules. Maturity calculations shown here are also based on the current bonus rates. It can also vary based on the actual performance of the corporation. For more details on risk factors, terms, and conditions, please read the policy documents carefully before concluding a sale.

FAQs on LIC’s New Endowment Plan

FAQs on LIC’s New Endowment Plan

Dummy

How much bonus is declared under the plan?

Is it possible to date back the policy?

What type of bonus is declared under the policy?

Does the plan provide a loan facility?

Are there any rebates on the premium?

The first on the high Sum Assured like 1.50% to 3%.

The second on premium paying Mode like 2% on Yearly or 1% on half-yearly mode.

Are riders available under the plan?

LIC's Market Share 75.9%, Growth in NB Premium 39.46%, Growth in 1st Year Premium 25.17%, Growth in Total Premium 12.42%, Growth in Gross Total Income 9.83%, Growth in Total Asset Value 2.71%, Growth in Digital Transaction 36% in FY 2019-20.

It also has a Claim Settlement ratio of 98.33%.

It is the most trusted Life Insurance Company in the country. It has a Sovereign Guarantee which other Companies don't have.

WHY GO SOMEWHERE ELSE?

WHY GO SOMEWHERE ELSE?

0 Comments